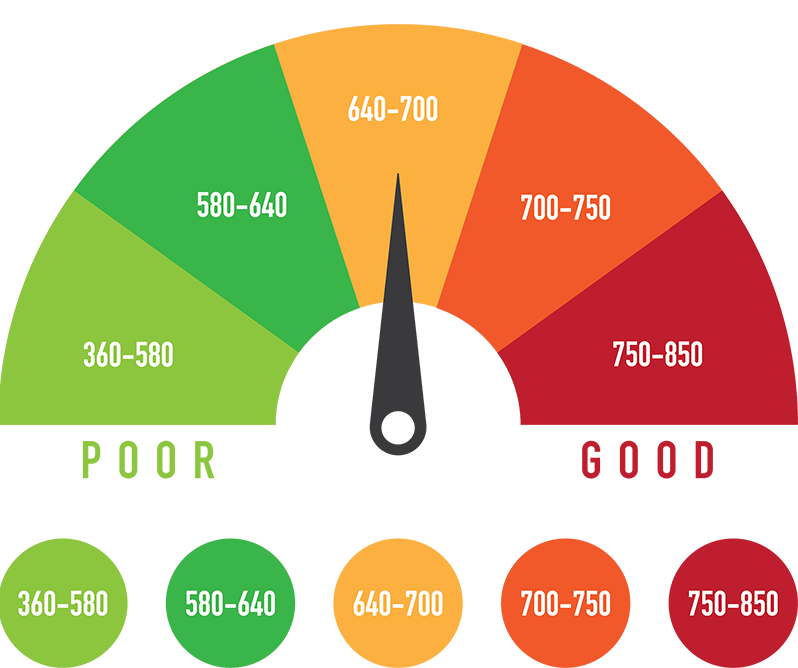

What are Credit Scores?

“A credit score is a numerical expression based on a level analysis of a person’s credit files, to represent the creditworthiness of an individual. A credit score is primarily based on a credit report, information typically sourced from credit bureaus” Source: Wikipedia

There are a few things you need to know about the credit scores. These are as follow:

1.Personal loans can save you a lot of debt you already have

The lower interest rates are one of the strongest benefits of using a personal loan. You could try these out reduce the amount of interest you pay and the time it takes to pay off the debt with lower rates. You could pay off unlimited rates on credit cards with a simple date of completion in mind.

2. Watch out for fees and extras

Many borrowers offer to cover or other additional costs if you close the mortgage. You might want or may not want an insurance policy to make sure that your creditors do not hold to your mortgage when the crisis hits, but that is not just because you have the idea that it is important for your loan, but a different financial decision that you have to make. (Walk away if the borrower wants it to be.)

3. Never get a personal loan to fund certain expenses

One of the nice things about a personal loan is that you don’t have to explain your investment from the borrower, unlike an auto loan or mortgage. There are items, though-whether with a credit card, credit line or personal loan-that you should know better than to pay for.

4.Pay off credit cards

One of the most common uses to combine existing debt for a personal loan, such as credit card balances, student loans or car loans. They may have an interest rate less than you have charged for your other loans and the organization’s advantage is that every month you have only one bill to pay. Nonetheless, you must move one type of loan to another. Bad credit isn’t a problem. Especially now that you can easily sign up for merchant accounts for bad credit. You could pay off unlimited rates on credit cards with a simple date of completion in mind.

5. A personal loan is not a long-term solution

Although regular mortgages are paid for over decades, personal loans usually only last seven years or fewer. You can’t borrow cash for more than you really need, so it can be a good thing. Nevertheless, it also ensures that if you want to spend a lot of money, such as a major home remodel, costs may be too high to keep yourself in line with your personal loan.

6. Money for moving expenses

Usually, local transfers aren’t costly. Nevertheless, a broad remote location may be costly enough to justify a personal loan, perhaps for an employment opportunity.